- Working Capital loan is a money borrowed for day to day business operations. This includes fixed regular expenses such as rent of the office ,factory , salary , labour wages . A working capital loan is not usually used to buy assets or make investments. However there is no restrictions on how to use the working capital loan once it is sanctioned to you.

S.M.E LOANS

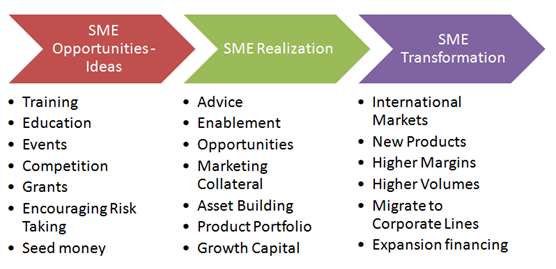

A business loan given to Small & Medium Size enterprises (SME’s) are known as SME Loans. These loans are offered to SME’s to meet their various requirements like setting up a unit, buying machinery, technology upgradation & other day to day working capital etc.…

As SME is the segment on which the economy of any country is based & as any business needs finance depending upon the size & nature of business, thus based on that there are Banks & NBFC’s who offers various types of SME Loans.

We at Financebay have encouraged our customers over the years. And now, we can propel your dreams. With us, you get quality service that is simple, friendly and customized. So, whatever the size of your business, the only question is how big do you want to be?

F.A.Q

What is the Working Capital loan ?

Why should I consider working capital loans ?

- Although your business may be running smoothly there will be lean periods when it won’t have the cash to cover immediate or short term costs. This could be because of delayed payments or unplanned expenditure. In this times working capital loans will help you meet daily expenses and grow your business without financial concerns.

Do I need to nominate a guarantor or attach security to qualify for this loan ?

- If it’s a Term loan bank will ask for security . Some products don’t need security or guarantor . Please contact FinanceBay loan advisor for more details .

What are the eligibility criteria for this loan ?

- Eligibility criteria for working capital loans are as follows.

You must a Self employed individual running a business from past 3 years.

Partnership , PVT Ltd , LLP and closely held limited companies are also eligible to apply.

Other applicants , depending on their profile are eligible on case to case basis.

Apart from this you must be an Indian national.

Do you pay interest on working capital loan?

- Like all business loans, working capital loans have an interest rate associated with them and the rate will vary from lender to lender. Usually, the interest rate on a working capital loan can be between 10 - 15% depending on the type of business you're running and how much you borrow.

How bank will decide the loan amount I am eligible for?

- BANK will decide the loan amount based on your repayment capacity. Repayment capacity takes into consideration factors such as income, age, qualifications, number of dependents, spouse’s income, assets, liabilities, stability and continuity of occupation and savings history. However, the eligibility of loan shall not exceed 50 -60 % of the cost of property.

Who can be co-applicant to the loan?

- You can include your spouse as a co-applicant for the Loan. His / her income can be added to enhance the loan amount. However, all co-owners of the property should necessarily be the co-applicant.

How will the rate of interest calculated?

- Interest is calculated on daily reducing balance. Your monthly out-go (equated monthly installment - EMI) is much lower as compared to the interest on annual reducing balance.

What is the tenure of the loan?

- Tenure of the loan depends up on the products like Termloan , Overdraft , Bank guarantee , Cash Credit etc You can repay the loan over a maximum period of 10 years. Repayment will not ordinarily be extended beyond the age of retirement (if you are employed) or on your reaching 60 years of the age, whichever is earlier. However, BANK will be endeavoring to determine the repayment period to suit your convenience.

What happens if working capital is negative?

- If working capital is temporarily negative, it typically indicates that the company may have incurred a large cash outlay or a substantial increase in its accounts payable as a result of a large purchase of products and services from its vendors.

How do I repay the loan?

- You repay the loan in Equated Monthly Installments (EMIs) comprising principal and interest. Repayment by way of EMI commences from the month following the month in which you take full disbursement.

Can I repay the loan ahead of schedule?

- Yes. You can repay the loan ahead of schedule.

Does the property have to be insured?

- You will have to ensure that the property is duly and properly insured for fire and other appropriate hazards, as required by BANK, during the tenor of the loan .

Whether a corporate enjoying a facility from a commercial Bank can apply for a loan?

- Yes. a company can have multiple banking facilities, i. e., Loans from two or more banks.

Can we take-over a loan with other commercial banks?

- Yes we can takeover loans from Banks / NBFC and Co operative banks and even can take top-up.